A Long Term Comparison of Tilting Strategies

A frequent debate among index fund investors involves “tilting” or over-weighting particular asset classes. Usually, the asset classes to be over-weighted are small cap and value stocks.

Some investors believe that a portfolio tilted towards small cap and value is superior to a market-weight portfolio. These investors believe that over-weighting these asset classes (relative to market-weight) and under-weighting other asset classes increases the likelihood of a superior outcome ( i.e. higher returns, lower risk, or both).

Other investors believe that a market-weight or TSM (Total Stock Market) portfolio is the best choice. These investors believe we don’t know which asset classes are most likely to outperform in the future, and that the market weights reflect the best balance of risk and reward given the information available to investors at any particular time.

Debates often involve detailed analysis of past performance which, of course, has only limited value for forecasting the future!

Nevertheless, even making apples-to-apples comparisons of past performance is complicated because “live” index funds which track the various asset classes have been available for a relatively short time.

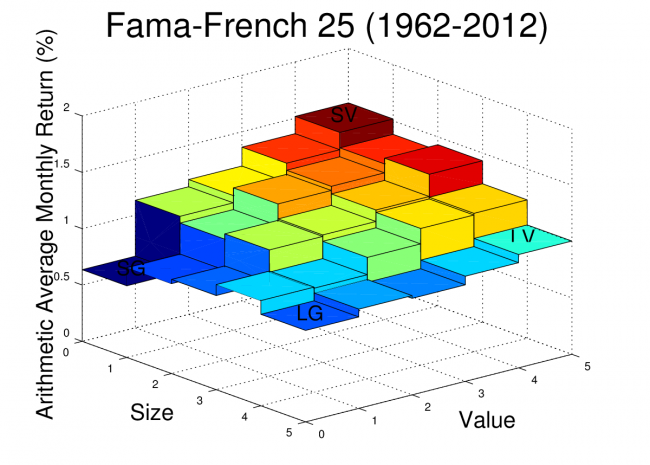

Academic datasets for TSM, small cap, and value indexes exist for longer periods of time (back to 1926 for U.S. stocks), but these indexes do not account for fund expenses and trading costs. Also, they sometimes involve extreme tilts toward illiquid stocks which are difficult for index providers to implement in practice.

In this post, I will evaluate the Fama-French factor loading for several “live” index funds, and I will then use the regression coefficients and alpha (which should capture expenses and other costs) to construct “pseudo-funds” which cover the full range of the academic data from to 1926 to present.

These pseudo-funds are an attempt to adjust the historical data for the expenses, trading costs, and modest factor loadings that we typically see with today’s live funds. The pseudo-funds can be used to compare realistic TSM and tilting strategies over an extended historical range.

Since we can’t know the future, I don’t think this post will settle the debate on tilting (No chance!), but this is my best attempt to look at the historical data through a fair lens.